5 Things You Should Know About Home Equity Lines of Credit

Table of Content

To find thebest HELOC rate, it's critical to compare multiple lenders — a rule of thumb is to get quotes from at least three so you can compare rates, fees and terms. You’ll also want to try improving your credit score, clearing out existing debt and making additional mortgage payments to increase your home equity. When theline of credit’s draw period expires, you enter the repayment period, which can last up to 20 years.

Each time you refinance, you pay additional fees and interest points. Because mortgage rates are currently among the lowest borrowing rates, refinancing can help you pay off higher interest rate debt and free up your cash flow. If you need to access additional funds, using the equity in your home can be a lower cost way to borrow the money compared to taking out a traditional loan or using a credit card. Some people aren’t comfortable with the HELOC’s variable interest rate and prefer the home equity loan for the stability and predictability of fixed payments and knowing how much they owe. It allows the borrower to take out money against the credit line up to a preset limit, make payments, and then take out money again. A home equity loan’s interest rate is fixed, meaning that the rate doesn’t change over the years.

How to Calculate Your Home Equity

During the draw period, you will make interest-only payments. During the repayment period, you will make principal-plus-interest payments. Since your home is collateral, if you don’t pay your HELOC back, you could risk foreclosure on your home.

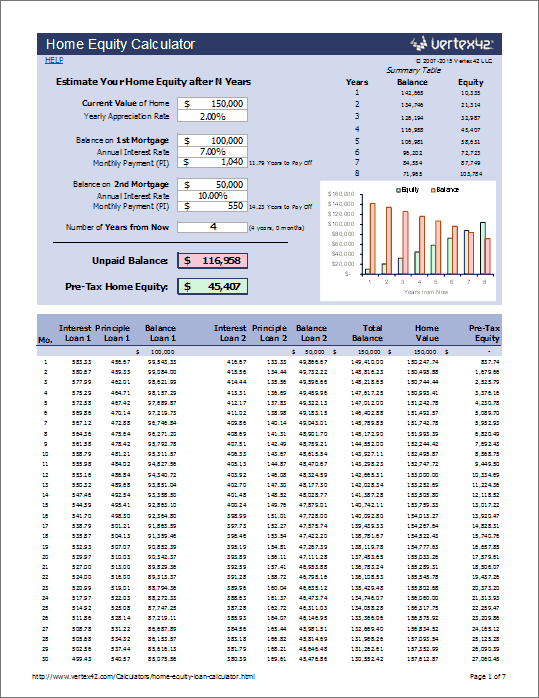

Your equity is the difference between what you owe on your mortgage and how much money you could get for your home if you sold it. High interest rates, financing fees, and other closing costs and credit costs can also make it very expensive to borrow money, even if you use your home as collateral. A home equity line of credit is a type of second mortgage, as is a home equity loan.

Debt Consolidation

Borrowers apply for a set amount that they need, and if approved, receive that amount in a lump sum up front. The home equity loan has a fixed interest rate and a schedule of fixed payments for the term of the loan. A home equity loan is also called a home equity installment loan or an equity loan. When you get a home equity loan, you receive a lump sum of cash up front. Most home equity loans have a fixed interest rate, where each monthly payment reduces your loan balance and covers some interest costs. The fixed rate home equity line of credit enables borrowers to set a part of the loan as fixed.

Acash-out refinancereplaces your current home mortgage with a larger home loan. The difference between the original mortgage and the new loan is disbursed to you in a lump sum. The maindifference between a cash-out refinance and a HELOCis that a cash-out refinance requires you to replace your current mortgage, while a HELOC adds a loan to your current mortgage. Large purchases - Because HELOCs have longer repayment periods than many loans, they may be an attractive choice for making large purchases.

Are HELOC interest rates higher than home equity or personal loans?

Secured by your principal residence; and the APR exceed certain threshold amounts that are tied to market conditions. If you have a high-cost mortgage, you may have additional rights under federal law, the Home Ownership and Equity Protection Act and theCFPB has more information about your special rights. If you decide not to take the HELOC because of a change in terms from what you expected, the lender must return all of the fees you paid.

Eight years later, the combination of the two HELOCs plus their mortgage gives them a balance of $250,000, and the house is now valued at $600,000. This means they can take out yet another HELOC for up to $297,500. The homeowner is now in the repayment period for that first HELOC, and in two years, the repayment period for the second HELOC will begin. Home equity lines of credit are based on the amount of equity you have in your home.

A home equity line of credit, or HELOC, could help you achieve your life priorities. At Bank of America®, we want to help you understand how you might put a HELOC to work for you. A HELOC is a line of credit borrowed against the available equity of your home. Your home's equity is the difference between the appraised value of your home and your current mortgage balance. Personal lending products and residential mortgages are offered by Royal Bank of Canada and are subject to its standard lending criteria.

Additionally, the fixed-rate option requires a $100 fee each time you lock or unlock a rate. PNC offers HELOCs, mortgage refinancing products and mortgage products. Its products and services vary by location, so you'll need to input your ZIP code on the website to see the rates and terms available to you. There’s a fixed interest rate, which means the payments won’t change over the life of the loan unless you make additional draws. With a HELOC, you borrow against your line of credit up to the limit and then pay back the amount you owe.

Unlike the continuous line of credit that comes with a HELOC, home equity loans work in much the same way as your first mortgage. To start, the funds from a home equity loan are disbursed in one lump sum. Additionally, these loans often come with fixed interest rates and fixed monthly payments. With a HELOC, you’re borrowing against the available equity in your home and the house is used as collateral for the line of credit. As you repay your outstanding balance, the amount of available credit is replenished – much like a credit card. This means you can borrow against it again if you need to, and you can borrow as little or as much as you need throughout your draw period up to the credit limit you establish at closing.

Also, the borrower has to pay an interest rate on the balloon amount that is usually variable. Due to varying home equity line of credit rates, the payment will differ monthly. On the failure of repayment, the borrower might also lose the house. However, the lender might not permit extra withdrawals if the house equity drops. After the draw period, the borrower has to pay off the balance loan amount within a certain timeframe.

You want to consolidate debt but don’t want to access a new credit line and risk creating more debt. Payments must be made on a HELOC during its draw period, which usually amounts to just the interest. With a HELOC, on the other hand, there’s no lump sum up front.

Comments

Post a Comment